July 15, 2026

The Hidden Infrastructure Behind Successful Investment Funds

Your fund's strategy only takes you so far. Discover the operational infrastructure that institutional investors evaluate before they commit.

Read More

Business

You are your business's most valuable asset. Every pitch, every client call, every late-night strategy session runs through you. Yet self employed health insurance remains one of the most overlooked pieces of founder protection.

Leaving a 9-to-5 means taking full ownership of your benefits package. The right business continuity planning starts with covering the person who keeps the lights on: You.

This guide breaks down every path to coverage, the tax deduction opportunities most founders miss, and how to turn your health plan into a wealth-building engine.

📖 YOU MIGHT ALSO LIKE

Think of health insurance as risk management for your company, not a personal expense. A single ER visit can cost $2,000 to $20,000 out of pocket. For a bootstrapped founder, that kind of hit drains capital earmarked for growth, hiring, or inventory.

In 2025, the average annual premium for family health coverage reached $26,993, a 6% increase from the prior year, according to KFF's Employer Health Benefits Survey.

Medical inflation keeps climbing, and founders without minimum essential coverage absorb every dollar of that risk personally. A medical emergency stalls product launches, delays payroll, and puts your entire operation at risk.

Over 72.9 million Americans now freelance in some capacity, according to MBO Partners, yet part-time workers are significantly more likely to be uninsured than their full-time counterparts, with 13% lacking coverage, according to KFF. That gap exists largely because most founders don't know where to start.

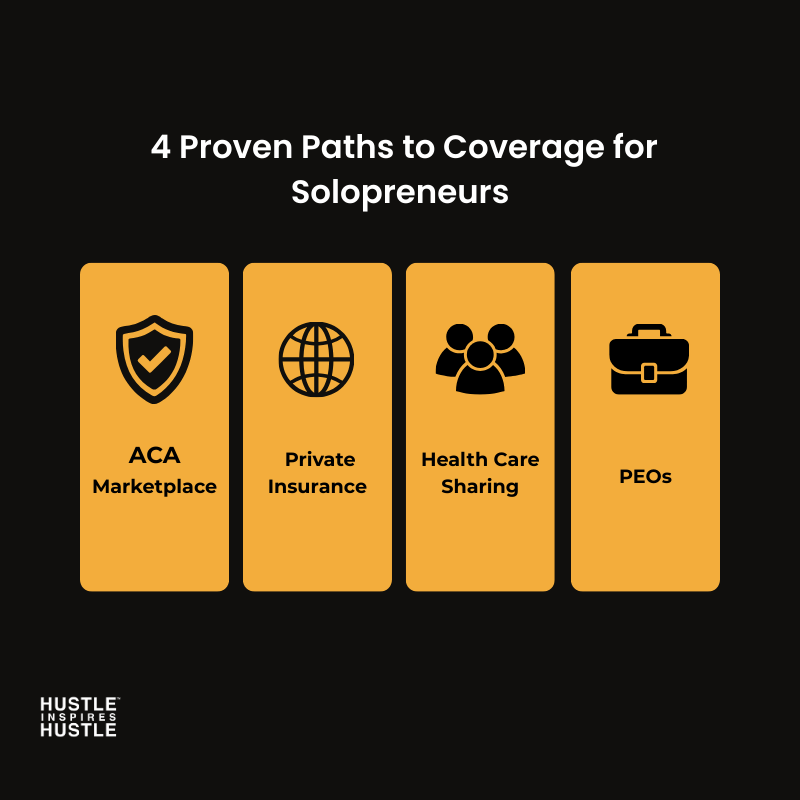

Choosing the right coverage depends on your hustle's current revenue and whether you prefer lower monthly premiums or broader doctor networks. Here are four reliable options for solopreneurs in 2026.

The ACA Marketplace at Healthcare.gov is the starting point for most self-employed founders. Unlike the employer plans, it’s open to anyone, and no carrier can reject you based on a pre-existing condition.

The real advantage here is the subsidy system: premium tax credits lower your monthly payment based on your estimated adjusted gross income. That matters when your income fluctuates quarter to quarter. Report accurate income projections upfront to avoid tax-time clawbacks. You will receive Form 1095-A at year's end to reconcile your credits with the IRS.

Private health insurance plans purchased off-exchange offer nationwide PPO networks and strong network adequacy. These are ideal for location-independent entrepreneurs who travel often and need access to top-tier specialists outside their home state.

Off-exchange plans also come with ancillary benefits like dental, vision, and telehealth bundles. You can explore global plan options if your hustle takes you across borders. The tradeoff: no premium tax credits apply to off-exchange purchases.

Health Care Sharing Ministries offer a budget-friendly, community-based alternative. Members contribute a monthly share that covers other members' medical bills. Organizations like AHCSM coordinate these programs.

HCSMs typically carry lower monthly costs, but they are not traditional insurance. Many don't cover pre-existing conditions, and there's no legal obligation for the group to pay a claim. This is a calculated risk with meaningful savings, best suited for solopreneurs in good health with emergency savings as backup.

Professional Employer Organizations use strength in numbers to unlock corporate-level group rates. By joining a PEO like Opolis or Freelancers Union, a solopreneur can co-employ themselves to access group health benefits, ancillary benefits, and 401(k) matching.

Network adequacy tends to be strong because PEOs negotiate with major carriers. For founders scaling toward their first hires, a PEO simplifies the jump from solo coverage to team benefits.

The self-employed health insurance deduction is one of the most powerful tax tools available to founders. You can deduct 100% of premiums paid for yourself, your spouse, and your dependents as an above-the-line tax deduction.

This reduces your adjusted gross income (AGI) directly, which means you pay less in federal income tax, potentially qualify for larger premium tax credits, and lower your self-employment tax base.

Every dollar your business spends on health premiums effectively earns a tax deduction. Track these expenses meticulously. Your CPA will thank you.

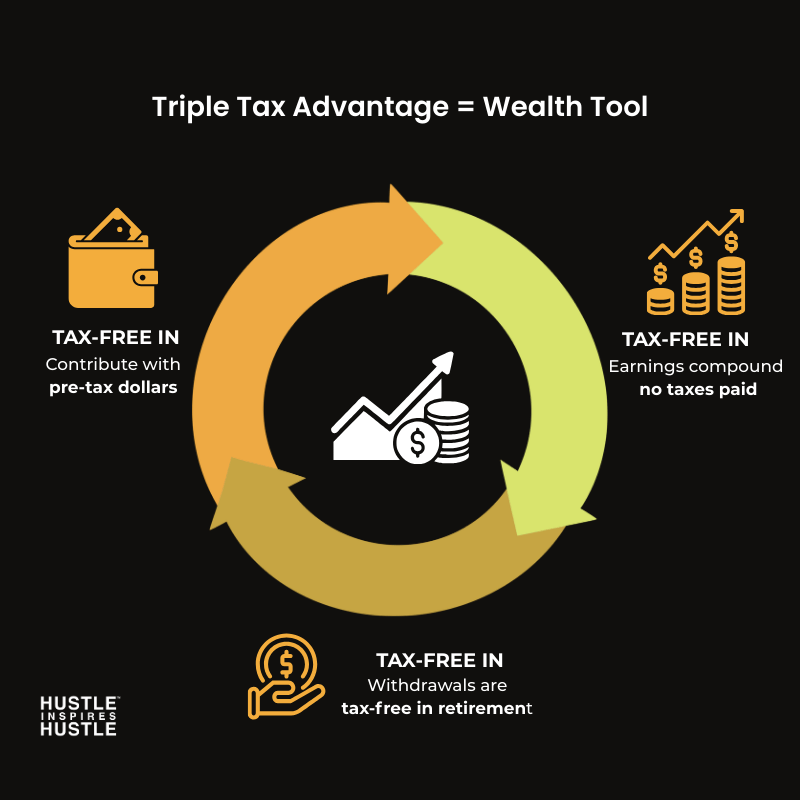

Pair a High-Deductible Health Plan (HDHP) with a Health Savings Account (HSA), and your medical plan becomes a secondary retirement vehicle. As of 2025, 33% of all covered workers are enrolled in HDHPs with a savings option, and the average HSA balance has risen to $5,457, an 11% year-over-year increase, according to SHRM.

The HSA's triple tax advantage makes it uniquely powerful. Contributions reduce your adjusted gross income, growth inside the account is tax-free, and withdrawals for qualified medical expenses carry zero tax deduction liability.

The strategy: pay small bills out of pocket and let HSA funds compound for decades. Learn more about how HDHPs and HSAs work together. The triple tax advantage makes an HSA one of the best financial tools a self-employed founder can access.

Scaling from a one-person show to a team creates new business continuity planning questions. ICHRAs (Individual Coverage Health Reimbursement Arrangements) offer a flexible path. They let you give employees tax-free money to buy their own plans on the ACA Marketplace or elsewhere, without you managing a group policy.

This approach keeps overhead low while providing your team with minimum essential coverage. Healthcare innovators like Charles Nader are building technology to make these transitions even smoother for growing companies.

These expensive lessons trip up founders every year. Avoid them to protect your cash flow and keep your hustle running.

The open enrollment window typically runs from November 1 through January 15. Miss it, and you're locked out of Marketplace coverage until the next cycle, unless you experience a qualifying life event like marriage, a move, or losing prior coverage.

If you miss the window and don't have a qualifying life event to trigger a Special Enrollment Period, your only immediate option is a short-term health plan. These carry lower premiums but typically exclude mental health care, prescription drugs, and maternity coverage entirely, leaving you exposed to the costs that matter most.

Set calendar reminders months in advance. Data-driven health tracking can also help you stay proactive about wellness, but it won't fix a missed deadline.

Your monthly premium tells only half the story. The out-of-pocket maximum is the true worst-case cost you could face in a plan year. This number determines how much liquid capital you need in your emergency fund. Some plans advertise low premiums but carry $9,000+ out-of-pocket caps.

Compare total potential costs across private health insurance and Marketplace options before you sign. Factor in ancillary benefits like prescription coverage and telehealth access when making your decision.

As your hustle scales and income increases, Marketplace subsidies decrease. Failing to report updated adjusted gross income leads to a surprise tax bill in April. The IRS will recalculate your premium tax credits based on actual income reported on your return, and any overpayment of credits gets clawed back.

Update your income estimate on Healthcare.gov whenever your revenue changes significantly. Reconcile everything using Form 1095-A at tax time. Treat this like bookkeeping: update monthly, not annually.

Your health plan is the foundation your business stands on. Audit your current coverage today. Compare your network adequacy, verify your tax deduction eligibility, and make sure your adjusted gross income projections align with what you've reported on the Marketplace.

A secure founder is a fearless founder, ready to take the big risks required to scale. Start building your protection plan now. Explore episodes from founders who've built resilient businesses and learn how they protect what matters most.

The ACA Marketplace at Healthcare.gov is the most accessible starting point. It offers plans with premium tax credits based on your adjusted gross income. Solopreneurs with higher incomes may also explore private health insurance or join a Professional Employer Organization to access group-rate coverage with stronger network adequacy and ancillary benefits.

At a minimum, you need a plan that qualifies as minimum essential coverage under federal guidelines. Many founders pair a High-Deductible Health Plan with an HSA for the triple tax advantage. Add liability and disability coverage depending on your industry. Review your out-of-pocket maximum and ancillary benefits to match your risk tolerance.

Claim the self employed health insurance deduction, which reduces your adjusted gross income dollar for dollar on premiums you pay. Maximize your HSA contributions for additional tax savings. Track every qualifying business expense, and work with a CPA who understands the nuances of the self employed health insurance deduction and quarterly estimated payments.

Start with health insurance that provides minimum essential coverage. From there, consider dental, vision, and disability coverage based on your lifestyle and revenue. Health Care Sharing Ministries offer a lower-cost alternative for generally healthy individuals. As your business grows, explore Professional Employer Organizations for group-rate benefits and ancillary benefits packages.

Alex Quin is a full-stack marketing expert and global keynote speaker. Founder and Chief Marketing Officer of UADV Marketing - a member of the Forbes Agency Council.