July 15, 2026

The Hidden Infrastructure Behind Successful Investment Funds

Your fund's strategy only takes you so far. Discover the operational infrastructure that institutional investors evaluate before they commit.

Read More

Business

It is 11:47 PM. You are refreshing your phone. Three Venmo notifications just hit from a client. A Stripe payout landed in the same account you use to buy groceries. Your partner asks what that $240 charge was, and you cannot remember if it was business or personal. April rolls around. Your accountant asks for a clean ledger. You freeze.

Sound familiar? This is how hustlers end up paying extra taxes, losing deductions, and in worst cases, getting their LLC veil pierced in a lawsuit. The fix is not complicated. You need a business checking account that actually works for the way you run your business.

This guide breaks down the best business bank account options for LLCs, sole proprietors, creators, and side hustlers in 2026. You will get honest comparisons on fees, features, APY, and which banks truly support the hustle economy. We are not here to sell you big bank fluff. This is real talk backed by real numbers.

Before we get into it, a quick heads up. Choosing the right business checking account aligns with your legal setup and tax strategy. If you want the bigger picture on setting up your business correctly, our guide to legal considerations for entrepreneurs is worth a read before you start applying.

A separate LLC bank account or business checking account is a non-negotiable infrastructure for any serious entrepreneur. It is not paperwork. It is not a formality. It is the financial foundation that protects your business, simplifies your taxes, and signals to the world that you mean business. Here is what it actually does for you.

Legal protection comes first. If you operate as an LLC and you mix personal and business funds, you risk piercing the corporate veil. A lawsuit or creditor can go after your house, your car, and your personal savings. That liability shield is the whole reason you formed the LLC in the first place. Do not wreck it by running everything through one personal account.

Tax simplicity is the next win. Separate accounts mean cleaner books, easier deductions, and fewer red flags if the IRS ever takes a closer look. Your accountant will thank you, and you will stop missing write-offs that were hiding inside a sea of mixed transactions. If you are still weighing whether to even hire a pro, check our breakdown on why startups need to invest in an accountant.

Credibility is the sneaky third benefit. Clients take you seriously when invoices come from a real business name. Vendors extend better terms. Partners trust you faster. And you need one to open a merchant account, apply for business credit, or qualify for future funding. Scale wants a real foundation. A proper startup bank account is that foundation.

LLCs and corporations need separate business accounts. Period. Mixing funds with an LLC bank account can destroy your liability protection in court. This is not a gray area for attorneys.

Sole proprietors are a different story. Technically, you are not legally required to open a business checking account for small business operations if you are a sole proprietor. Practically, you still should. Separate sole proprietor banking makes taxes cleaner, business credit building possible, and your books actually usable.

IRS Publication 583 states that one of the first things you should do when starting a business is open a business checking account and keep it separate from your personal account. The line between "should" and "must" is thinner than most new hustlers realize.

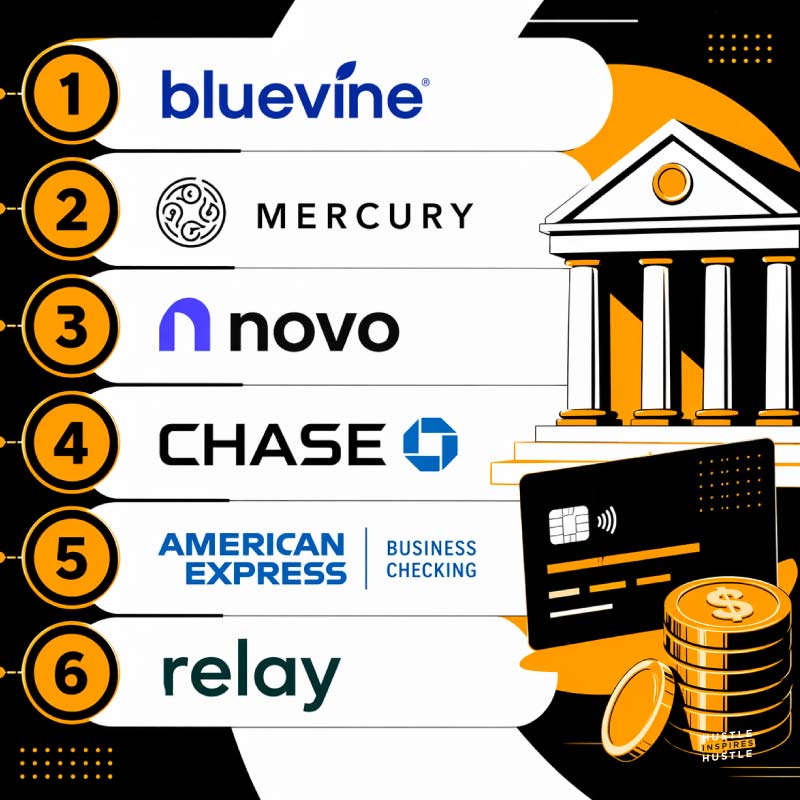

Let us get into the comparison. These are the top picks for the best business bank account in 2026, ranked by real-world fit for entrepreneurs at different stages. This business account comparison covers fees, features, and who each account serves best.

Bluevine Business Checking leads the pack for interest-earning hustlers. No monthly maintenance fee on the Standard plan, no minimum balance requirements, and up to 1.3% APY on balances up to $250,000 if you meet light monthly activity. The Plus plan pushes that to 1.75% APY, and Premier hits 3.0% APY on balances up to $3 million.

The catch on upper tiers is higher fee thresholds to waive, but the Standard plan stays free. Best for bootstrapped founders, service businesses, and LLCs who want yield without fee headaches.

Mercury is the tech-startup favorite. No monthly fees, no minimum balance, and unlimited transaction limits. Mercury also offers up to $5 million in FDIC coverage through their sweep program and strong treasury features for founders parking serious cash. API access, multi-user controls, and modern expense tools make it a go-to for digital and venture-backed businesses. Mercury integrates natively with QuickBooks, Xero, Stripe, and other platforms, so your bookkeeping software stays in sync from day one. Best for tech startups, digital agencies, and scaling operators.

Novo keeps it simple. Zero monthly fees, free ACH payments, and a clean mobile app that creators and solopreneurs love. Novo does not pay interest on balances, which is the main trade-off. Best for: freelancers, creators, and simple solo LLCs who want a fast setup with no surprise charges.

Chase Business Complete gives you the traditional option. Monthly fee around $15, waivable with a qualifying balance. You get thousands of physical branches and ATMs, easy cash deposits, and full banking services under one roof. Chase also offers access to business credit lines and relationship bankers, which matters when you are ready to borrow or expand operations.

Best for retail, cash-heavy businesses, or founders who want relationship banking and the option of a local branch.

American Express Business Checking rewards spending. 1.30% APY on balances up to $500,000, no monthly fees, and Membership Rewards points for AmEx loyalists. This is the account for founders who want their everyday entrepreneur banking to feed directly into a rewards strategy without juggling multiple platforms. Best for founders already in the AmEx ecosystem who want their checking to fuel their rewards game.

Relay rounds things out. Built for Profit First fans and multi-account organization nerds. Free, no fees, and lets you run up to twenty business checking account sub-accounts for clean cash flow management.

Relay is especially useful for agencies and service businesses that need to separate operating funds, tax reserves, and project budgets inside one dashboard without any additional monthly cost. Best for operators using the Profit First method and agencies juggling project funds.

If you want the best online business bank account with zero monthly cost, the short list is Bluevine Standard, Mercury, Novo, and Relay. All four give you no-fee business checking with no minimum balance traps. What you give up is usually easy cash deposits or physical branches. What you gain is every dollar of your revenue staying where it belongs, in your account.

Bluevine edges out as the top no fee business checking pick because you earn yield while paying nothing. Mercury wins for startups wanting serious FDIC insured coverage through sweep accounts. Novo wins for simplicity. Relay wins for operators who love structure.

Parking your operating cash in a zero-interest checking account in 2026 is leaving money on the table. The best business bank account for small business owners with cash reserves should pay you something. Bluevine Premier leads with 3.0% APY.

American Express Business Checking pays 1.30% APY. Mercury does not pay APY on checking, but offers Mercury Treasury, which can push funds into interest-bearing market products. The smart play is to stack. Use a yield-paying checking account for operating capital and a separate business savings account for larger reserves, when it fits.

The divide between online-first fintechs and brick-and-mortar banks is the biggest fork in the road for new entrepreneurs. Neither option wins on paper. It depends on how you actually run your business.

Online business banking wins on fees and user experience. Mercury, Bluevine, Novo, and Relay give you faster onboarding, better mobile business banking, modern integrations, and slick dashboards. You can open an account from your phone in under ten minutes. Features like instant notifications, expense categorization, and QuickBooks integration save hours. Online business banking is built for digital entrepreneurs, creators, and service businesses that live online anyway. Great mobile business banking also means you never lose a receipt again, since everything syncs automatically.

Most side hustlers and digital-first founders will never need to walk into a bank branch. If your payments come through Stripe, your invoices go out digitally, and your receipts live in an app, an online account handles everything better and cheaper.

Traditional banks still matter for a few reasons. If you run a cash-heavy business, restaurant, barbershop, or retail shop, you need physical cash deposits without trekking to Walmart. If you want a relationship banker for future loans, local institutions beat fintech every time. If you value face-to-face service when something goes wrong, a branch wins. Chase, Bank of America, and Wells Fargo lead here.

Plenty of founders run a hybrid setup. Use an online business banking account like Bluevine or Mercury for daily operations and a traditional bank for handling cash deposits or applying for a business credit line. This small business banking combo gets you the best of both worlds without forcing a single choice.

Picking the right account depends on three things. What kind of business do you run? How much is moving through your accounts each month? What stage are you in?

E-commerce and digital businesses need strong payment integration. Stripe, PayPal, Shopify, and Square integrations should sync automatically. Service businesses need simple invoicing, unlimited ACH payments, and clean reporting. Retail or cash-heavy operations need a traditional bank that accepts cash deposits without drama.

A new side hustler testing the waters can start with a free Novo or Bluevine Standard account. A scaling LLC pulling $50K+ per month should look at Mercury or Bluevine Plus for better features and support. An established business with employees and inventory might need a traditional institution for payroll, wire transfers, and credit lines. International wire transfers get expensive fast, so if you send them regularly, factor in per-transaction fees when comparing.

Some accounts cap monthly transaction limits or charge per transfer after a threshold. High-volume businesses should prioritize unlimited transactions. If you work with international clients regularly, check for multi-currency support or competitive wire transfer rates. International wires can run $20 to $50 per transfer at traditional banks, which adds up fast if you send them frequently. Run the numbers against your real cash flow patterns, not a best-case projection.

If you are still figuring out what business to build before opening your account, our roundup of side hustles for women is a solid place to start.

For LLCs wanting an LLC bank account without monthly costs, the three standouts are Bluevine Standard, Mercury, and Novo. All three accept LLCs, require EIN documentation as part of the application process, and charge zero monthly fees. Opening any of them takes about fifteen minutes online. You will need your EIN confirmation letter, your LLC formation documents (Articles of Organization), your operating agreement, and a government-issued ID. That is it.

First-time LLC owners often overthink this step. Do not. The process is genuinely simple. You will need your EIN confirmation letter, your LLC formation documents, your operating agreement, and a government-issued ID. That is it. Gather those documents before you start the application, and you will breeze through it.

Fees and APY are not the whole story. Before you commit, check these six features against your actual business needs. This is how the best banks for business accounts separate themselves from the pack.

ACH payments and wire capabilities. Free ACH payments should be standard. Wire fees vary wildly, so check the fee schedule for both incoming and outgoing. International wires can run $20-$50 per transfer at traditional banks.

Here are four mistakes we see all the time. Each one costs money, time, or both. Avoid these, and you are ahead of most other founders in the small business banking game.

This is the biggest and most common error. Mixing funds creates tax chaos, kills your legal protection, and makes bookkeeping a nightmare. Open a real business checking account for your business operations on day one. The top-rated options for this are free. There is no excuse.

Monthly fees, wire fees, ATM fees, and overdraft fees add up fast. A "free" account with $30 in hidden transaction fees monthly costs you $360 per year. Read the full schedule before signing up. Compare the annual cost against your realistic usage.

A $500 welcome bonus is nice. Paying $25 monthly fees for the next five years is not. Prioritize fit over flash. Some of these best banks for business accounts offer strong ongoing value, not just one-time hype. Your goal is to stop searching and start building. Pick the right small business banking partner and move on.

Minimum balances, monthly deposit thresholds, and debit card spend requirements can all trigger fees. Choose accounts aligned with your actual cash flow. If you are new and bootstrapped, do not pick an account that requires a $10,000 minimum to waive fees. If you cannot meet the bar, the account is not free.

Picking the best business bank account is a strategic move, not a formality. The choice impacts your daily operations, tax season, legal protection, and growth potential. You are going to interact with this account every single day. Get it right.

Here is the short recommendation for each audience. Bootstrapped side hustler, go with Novo or Bluevine Standard. Scaling LLC, Mercury, or Bluevine Plus. Cash-heavy or retail business, Chase Business Complete, or a regional traditional bank. Creator or freelancer running side hustle banking operations, Novo or Bluevine.

Here is your move. Pick one account from this guide that fits your current stage. Open it this week. Redirect incoming payments starting next week. Move recurring business charges over the following week. Thirty days from now, you will have clean books, real legal protection, and one less thing mixing with your personal life. That is how you protect the hustle.

Ready to keep leveling up? Check our list of the best entrepreneur books to sharpen your next move, or explore side hustles for women if you are scouting what to launch next.

Stop mixing money. Protect your hustle. Open a real business account today.

Legally, no, but practically yes. Sole proprietors are not required by law to open a separate business checking account, but mixing personal and business funds creates tax headaches, kills credibility, and makes bookkeeping nearly impossible. Opening a free account like Novo or Bluevine takes fifteen minutes and protects your hustle from day one.

Bluevine and Mercury top the list for LLCs wanting zero fees. Bluevine offers up to 1.3% APY on balances with light activity requirements, unlimited transactions, and no minimums. Mercury delivers powerful startup features, API access, and up to $5 million in FDIC-insured coverage. Both accept LLCs, and both require just your EIN to open.

Technically possible, financially risky, legally dangerous. Using a personal account for your LLC can pierce the corporate veil and expose your personal assets in a lawsuit. The IRS flags commingled funds as a red audit signal, too. Open a proper LLC bank account immediately. It protects your business, your personal wealth, and your peace of mind.

Costs range from $0 to $100, depending on the bank. Online-first options like Bluevine, Mercury, and Novo charge nothing to open and have no monthly fees. Traditional banks like Chase or Bank of America typically require $25 to $100 as an opening deposit and charge $15 to $30 monthly unless you meet waiver requirements. For bootstrapped entrepreneurs, the best bank account for small business operations is almost always one of the free online options.

Alex Quin is a full-stack marketing expert and global keynote speaker. Founder and Chief Marketing Officer of UADV Marketing - a member of the Forbes Agency Council.