August 1, 2026

The Hidden Infrastructure Behind Successful Investment Funds

Your fund's strategy only takes you so far. Discover the operational infrastructure that institutional investors evaluate before they commit.

Read More

Business

Gross pay vs net pay is an important concept to understand when it comes to managing your finances. Knowing the difference between gross and net income can help you better plan your budget, save money, and understand how payroll taxes affect your take-home pay.

In this article, we will explain what gross pay and net pay are, their differences, and why they're important to know. By the end, you'll have a deeper understanding of how your earnings work and what factors contribute to your overall income.

📖 YOU MIGHT ALSO LIKE

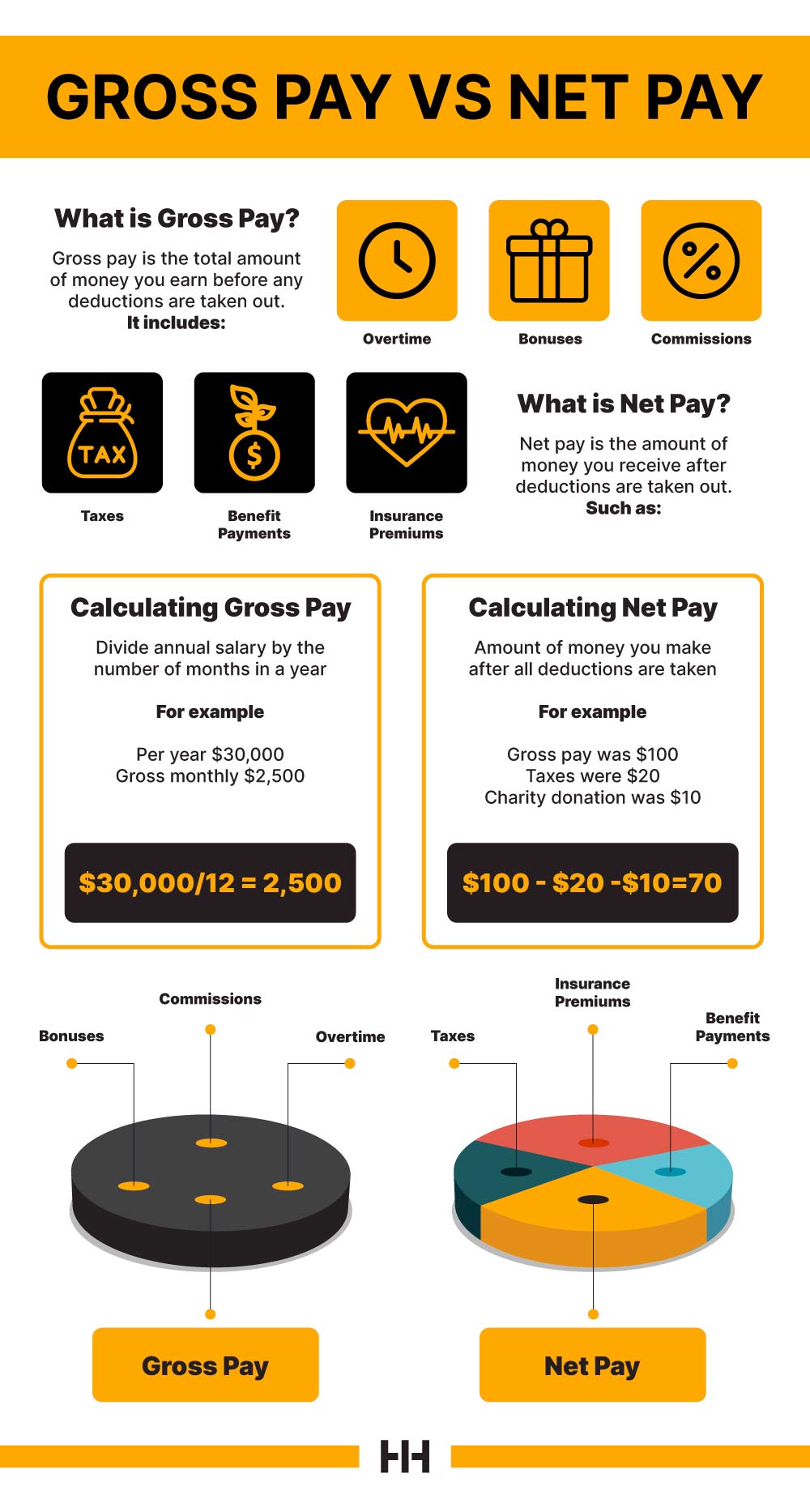

What is gross pay? Gross pay is the total amount of money you earn before any deductions are taken out. It includes your standard salary plus any additional earnings such as 4 This is also known as gross income.

Gross pay is important to understand because it's the figure used when calculating your total income for tax purposes. It's also helpful to know since it can give you an idea of how much money you will have coming in each month, and it can help you budget accordingly.

What is net pay exactly? Net pay is the amount of money you receive after deductions such as taxes, benefit payments, and insurance premiums are taken out. This figure is sometimes referred to as take-home pay or net income. Understanding your net pay can help you plan for bills, spend money, and save for the future. It's also important to consider that your net pay can change if you work overtime or receive a bonus, as deductions will be taken out of this additional income.

Hourly pay simply means that you are paid a set hourly rate for the number of hours you work. To calculate gross wages for hourly employees, simply multiply their hourly wage by the number of hours they worked. For instance, if an employee works 25 hours per week and earns $12 per hour, their gross weekly pay would be $300 (25 x 12 = 300).

Salary pay is a predetermined amount of money earned over a certain period of time (usually per month or year). To calculate gross wages for salaried employees, simply multiply their annual salary by the number of months in a year. For example, if an employee earns $30,000 per year, their gross monthly pay would be $2,500 ($30,000/12 = 2,500). If an employee is paid bimonthly and earns $60,000 per year, their gross wage per pay period is $60,000 ÷ 24 = $2,500. Add bonuses and commissions.

The FLSA states that to calculate overtime pay for nonexempt employees, you need to multiply their regular rate of pay by 1.5 and the number of overtime hours worked( In excess of 40 hours a week). However, some states have different requirements, like double time, which benefit the employee even more.

Taxes are government-mandated deductions that everyone must pay. Different taxes include Federal Income Tax, as well as Social Security and Medicare taxes. To calculate the Federal Income Tax (FIT) for an employee, we use the information from their completed W-4 form, their taxable wages, and pay frequency. The two methods used to calculate FIT are the Wage Bracket Method and the Percentage Method, as described in Publication 15-T (2022) on Federal Income Tax Withholding Methods.

The funding for Social Security comes from a specific payroll tax. This tax is split between employees and employers, with each party contributing 6.2 percent of their wages (up to a maximum of $160,200 in 2023). However, self-employed individuals pay the entire tax themselves at a rate of 12.4 percent. These tax rates are established by law and only apply to earnings up to a certain threshold for OASI and DI. Medicare taxes are also taken out of employees' wages and split between employees and employers at a rate of 1.45 percent each.

Benefits one can receive from their employer vary by company, but some common employee benefits are health insurance and retirement plans. Employers may offer these types of benefits to employees as part of the overall compensation package. Benefits are typically deducted from an employee's gross pay before taxes, so they may not realize how much money is actually being taken out for these purposes.

To calculate the amount of money deducted for benefits, employers must first determine how much the employee's cost is for each benefit. From there, they can calculate the total deduction by adding up all individual benefits and multiplying them by the number of pay periods per year.

Other deductions may be taken out of an employee's gross pay, depending on the employer. Some common examples are union dues, garnishments (for unpaid debts), and voluntary contributions to charities or other organizations. Employers can deduct these amounts from their employees' gross wages after taxes have been calculated and prior to issuing the check or direct deposit.

Gross pay is an important part of understanding your income and budgeting appropriately. Calculating gross wages correctly is critical to making sure employees are paid accurately and on time. It's also essential for employers to follow the guidelines set forth by state and federal regulations when it comes to payroll taxes, deductions, and other obligations. By understanding how to calculate gross wages and accurately deduct taxes, employers can ensure their employees are paid correctly and that they remain compliant with applicable laws.

Now, we will be moving on to net pay. Net pay is the amount of money an employee actually takes home after deductions are taken out for taxes, benefits, and other items.

It is important for employees to understand their net pay for a number of reasons. Budgeting and financial planning are two of the most important reasons. Knowing how much money an employee will be taking home each pay period can help them plan out their monthly budget in order to ensure they are not overspending or falling short of their income goals. It is also important to be aware of any deductions that are taken out since these deductions can vary from paycheck to paycheck.

To calculate net pay, you must first figure out your gross pay. That is the amount of money you make before any deductions are taken out. Then, subtract taxes, benefits, and other deductions like union dues or charitable contributions from your gross pay. The number you get is your net pay - this is the amount of money that goes into your bank account. For example, if your gross pay was $100 and taxes were $20, and a charity donation was $10, then your net pay would be $70 ($100 - $20 -$10). This is just a basic example, but it illustrates how deductions from gross pay can affect the amount of money an employee takes home.

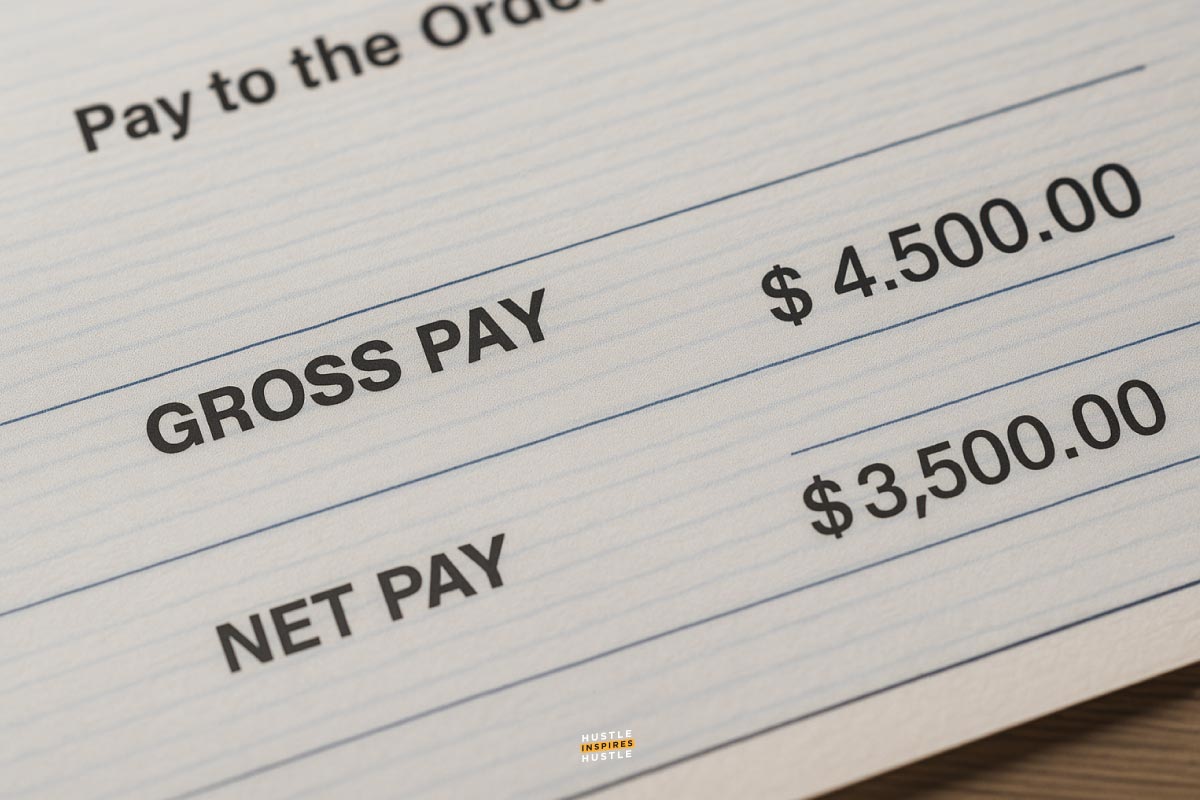

There are some key differences between gross and net pay, the most important being that net pay is the amount of money that an employee actually takes home after deductions for taxes, benefits, and other items have been taken out, while gross pay is the amount of money earned before any deductions are made. It is important to understand these differences in order to budget appropriately and make sure that you are not overspending or falling short of your income goals.

This section will discuss common gross vs net pay scenarios:

Salary employees are those who are paid a fixed amount of money regardless of the number of hours they work. This means that their gross pay is usually the same each month, so employers can calculate it easily by multiplying their salary by the number of pay periods in the year. For example, if an employee earns an annual salary of $50,000 and is paid bi-weekly, then their gross pay per paycheck would be $1,923.08 ($50,000/26).

Hourly employees are paid according to the number of hours they work, meaning that their gross pay can vary from paycheck to paycheck. To calculate the gross pay for an hourly employee, employers must calculate the number of hours worked, multiply it by the worker's hourly rate, and then subtract any deductions that need to be made. For example, if an employee works 40 hours a week and earns $15 per hour, then their gross pay for that week would be $600 ($15 x 40).

Commissioned employees are those who receive a percentage of the profits from their sales. Wage calculations for this kind of employee can be more complicated than for salary or hourly employees since their gross pay will vary depending on the number of sales they make. To calculate the gross pay for a commissioned employee, employers must add up all of their commissions from the period and subtract any deductions that need to be made.

Gross pay and net pay are two different amounts of money that employers must calculate when paying their employees. Gross pay is the amount of money earned before any deductions are made, while net pay is the amount of money an employee actually takes home after taxes, benefits, and other deductions have been taken out. It is important for both employees and employers to understand the differences between gross pay and net pay in order to budget appropriately and make sure they are not overspending or falling short of their income goals.

Elevate your entrepreneurial game with actionable advice and inspiring interviews from high-level entrepreneurs, business owners, and overall badasses in the game. Get more insight and inspiration on our blog posts, podcast episodes, or invite-only community.

Net pay vs gross pay, which is better? While both net pay and gross pay are important, net pay is typically more important to employees since it is the amount of money that actually goes into their bank accounts.

Your net pay is the amount of money that goes into your bank account after taxes, benefits, and other deductions have been taken out.

Put simply, gross wages are the total amount of money earned before any deductions are made.

To calculate gross earnings or salary, employers must multiply the employee's salary by the number of pay periods in the year.

The term "income" includes all forms of payment, such as cash, dividends, shares, profits, etc. "Salary" specifically refers to the payment an employer gives to an employee in exchange for work done.

Net pay is calculated by subtracting any deductions that need to be made from the gross pay. This includes taxes, benefits, and other items such as 401k contributions.

Alex Quin is a full-stack marketing expert and global keynote speaker. Founder and Chief Marketing Officer of UADV Marketing - a member of the Forbes Agency Council.